Investing Is No Longer “Rich People Stuff”

This Beginner’s Guide to Investing in 2026 (Gen-Z Edition) is designed for young people who want to start investing confidently even with little money and zero experience.

If you’re 18–30 and thinking:

“I should probably start investing, but I have no idea where to begin”, this guide is for you.

We understand that investing can seem complex, but this guide cuts through the noise, offering step-by-step strategies and clear explanations to help you confidently navigate the markets, select the right assets, and secure your long-term goals in the year 2026.

Investing in 2026 isn’t just for rich people or finance experts. With a phone, a small amount of money, and the right knowledge, you can start building real wealth early, and future you will be extremely grateful.

This beginner’s guide to investing in 2026 breaks everything down in simple terms: what investing is, where to start, what to buy, and how to avoid the mistakes that wipe out beginners.

You don’t need:

- a finance degree

- a big salary

- insider info

You just need:

- consistency

- basic knowledge

- patience

What Is Investing? (No complicated talk)

Investing = putting your money into things that grow or pay you over time instead of letting it sit and lose value.

Think of it as:

planting money today so it grows into more money tomorrow.

Instead of:

saving money → losing value to inflation

You:

invest money → money grows → future freedom

Common investments include:

- Stocks (owning a piece of companies)

- Bonds (lending money to governments or companies)

- Index funds / ETFs

- Money Market Funds

- Real estate

- Crypto (high risk)

- Treasury bills & bonds

Goal: long-term wealth, not quick wins.

The Mindset You Need Before Investing 🧠

1. Starting early is unfairly powerful

Your biggest advantage isn’t salary.

It’s time.

Thanks to compounding (money making money), starting in your 20s can literally double or triple what you end up with compared to starting later.

Someone investing KSh 5,000 monthly from age 22 can end up 2–3x richer than someone starting at 30.

Example:

- Invest $5,000 + $200 monthly

- Average return: 7%

After 30 years → $204,000

Start 5 years later → $138,000

Same effort. Huge difference.

If you delay by 5 years, with the same contributions and return rate, you’d end up with approximately $138,000, a difference of $66,000 simply because you waited.

This illustrates how time in the market, even more than how much you start with, can be your greatest advantage.

Time = power.

Time beats talent.

2. Inflation is silently robbing you

If inflation = 7%

Your savings account = 3%

You’re losing 4% every year.

In contrast, investing in assets that have historically outperformed inflation, such as stocks or inflation-protected bonds, helps preserve and increase your real purchasing power.

3. Know your time horizon

- Short (0–5 yrs): emergency fund, gadgets, travel

- Medium (5–15 yrs): business, land, house

- Long (15+ yrs): retirement, freedom

Your time horizon influences the risk level you can afford to take. Longer horizons typically allow for more aggressive strategies because temporary market fluctuations have time to even out.

Longer time = more risk allowed.

Know Your Investor Type: Goals + Risk + Time

Ask yourself:

What am I investing for?

- Freedom

- Business

- House

- Retirement

- Travel

How would I react if my investment dropped 20%?

- Panic and sell

- Be stressed but wait

- Buy more

This helps classify you as:

- Conservative – prioritize capital preservation.

- Moderate – balanced growth and stability.

- Aggressive – long-term growth with higher volatility.

Most Gen-Z investors are naturally moderate to aggressive because of long time horizons.

Money Basics First (Don’t Skip This)

Emergency fund

Before heavily investing, build a cash buffer of 3–6 months’ living expenses.

Save 3–6 months of expenses in:

- Money Market Fund (best)

- or bank account

This ensures that if unexpected costs arise (such as job loss or medical bills), you don’t have to liquidate your investments at an inopportune moment.

In other words, the Emergency Fund protects you from selling investments when life happens.

Debt Management

Kill high-interest debt

High-interest debt like credit cards should generally be paid down before investing heavily.

Mobile loans & credit cards = 20–40% interest.

Pay them off before heavy investing.

The “guaranteed return” of paying off, say, a 20% interest rate credit card is often better than speculative stock market returns.

Where to Invest in Kenya in 2026 (Beginner-Friendly Options)

Popular beginner-friendly options:

Local platforms

- Hisa App (stocks & ETFs)

- Ndovu Wealth (Robo Investing-Managed portfolios)

- Abacus

- CBK DhowCSD (government bonds)

Money Market Funds

- CIC

- Britam

- ICEA Lion

- Sanlam

Account types explained

- Money Market Fund → safe, good for emergency fund

- Brokerage account → stocks, ETFs

- Pension / Individual Pension Plan → long-term retirement

- Treasury bonds & bills → stable income

Robo-Investing vs DIY

Robo-advisors (Ndovu etc.)

- Easy

- Automated

- Beginner friendly

- Small fee

DIY investing

- More control

- More learning

- Lower fees if done right

Both are okay.

NOTE:

- Robo-Advisors: Great for beginners who want a hands-off experience. They build, rebalance, and manage your portfolio for a small fee.

- DIY Investing: For investors who enjoy choosing their own funds and individual stocks. Offers more control and potentially lower cost (if you pick low-cost funds), but requires more effort and discipline.

Beginner Investment Glossary (No boring stuff)

- ETF – basket of many stocks

- Index fund – tracks the market

- Dividend – money companies pay you

- Volatility – price going up and down

- Expense ratio – fund fees

- Diversification – don’t put all money in one thing

- Asset Classes: Different types of investments, like stocks, bonds, real estate, and cash.

- Yield: The income (usually from dividends or interest) earned on an investment.

- Expense Ratio: The annual fee charged by mutual funds or ETFs, expressed as a percentage.

- Price-to-Earnings (P/E) Ratio: A valuation metric that compares a company’s stock price to its earnings per share.

- Market Order: Buying or selling an asset immediately at the current market price.

- Limit Order: Buying or selling at a specific price or better.

- Stop-Loss Order: Automatically selling a security when it drops to a predefined price to limit losses.

Best Investments for Beginners in 2026 📈

1. Index Funds & ETFs (your main weapon)

These own hundreds or thousands of companies.

Why they’re perfect:

- Low cost

- Low effort

- Diversified

- Historically strong returns

Examples:

- S&P 500 ETFs

- Total World ETFs

- Emerging Markets ETFs

2. Individual stocks (small portion)

Use 90/10 rule

A simple rule for beginners: allocate 90% of your portfolio to funds (like index funds) and reserve 10% for individual stocks. This balances diversification with the opportunity for higher growth (and risk).

- 90% funds

- 10% stocks

What to check:

- Growing Revenue: Is the company growing its sales over time?

- Profit: Are profits increasing, and is profit margin stable or improving?

- Debt (Low debt): How much leverage is the company using? High debt can be risky.

- Strong Brand (moat)

The “Moat” Concept

A “moat” is a long-term competitive advantage. Think of things like:

- Strong brand (e.g., Apple)

- Network effect (e.g., social media platforms)

- Cost advantage (e.g., firms with efficient production)

Companies with moats are often better positioned to maintain profitability over time.

3. Bonds & Treasury securities

BOND – Money lent to a government or a company.

Bond – Money lent to a government (through Central Bank of Kenya) or a company.

Less risky. More Stable.

Good for:

- Balancing risk

- Income

- Preserving capital

Kenya:

- Treasury bills (91–364 days)

- Treasury bonds (2–30 years)

4. REITs (Real Estate Investment Trusts)

Earn rental income without buying property.

Good diversification.

5. Crypto (small only)

Max 1–5% of portfolio.

Focus on:

- Bitcoin

- Ethereum

High risk. Long-term mindset only.

2026 Market Trends to Know

AI

Stop guessing stocks, instead look at these;

- Growing AI ETFs

- Automation stocks

- Cloud infrastructure

Climate & green finance

- Carbon markets

- Clean energy

- Green bonds

Tokenized assets

Real estate & bonds on blockchain.

Emerging markets (Africa and Asia Growth)

- Kenya fintech

- Vietnam

- Indonesia

Beginner’s Guide to Investing in 2026: Smart Strategies That Actually Work🎯

Asset allocation

Here are sample models depending on your risk profile:

| Investor Type | Suggested Allocation |

| Aggressive | 80% Stocks / 20% Bonds |

| Moderate | 60% Stocks / 40% Bonds |

| Conservative | 40% Stocks / 60% Bonds |

Consider a portion in global equities or real assets (REITs) for diversification.

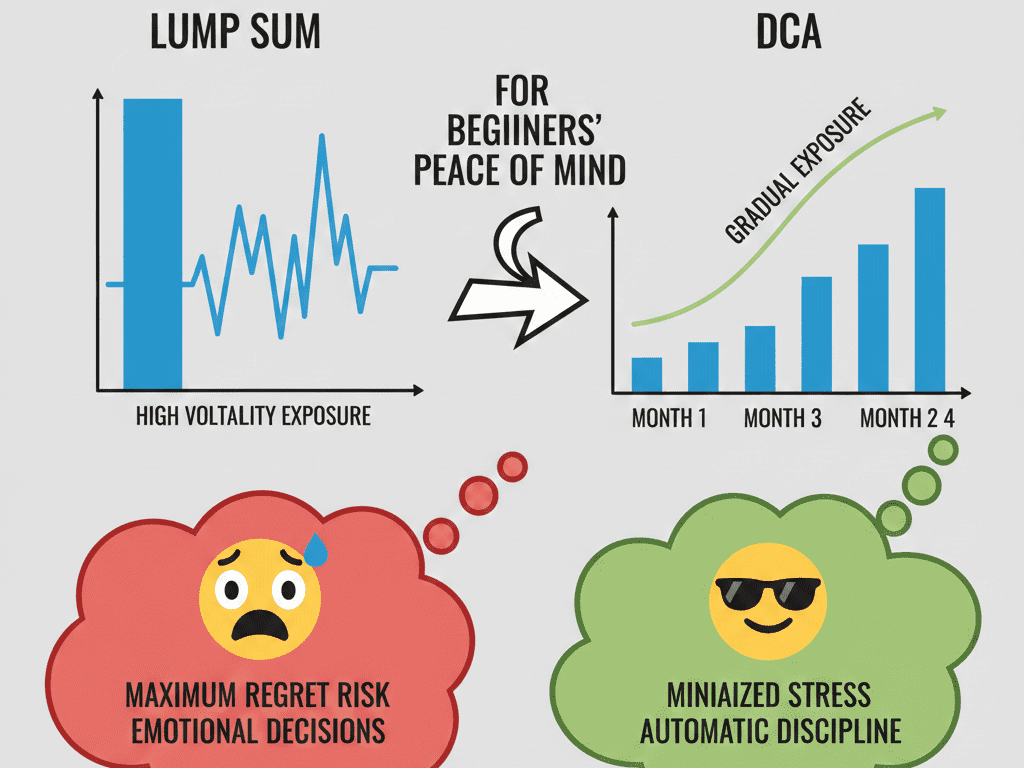

Dollar-Cost Averaging (DCA)

Invest same amount monthly.

Removes fear.

What is DCA?

Dollar-cost averaging means investing a fixed amount of money at regular intervals (e.g., monthly), regardless of market conditions.

Perfect for:

- students

- first jobs

- side hustlers

DCA vs. Lump Sum

- DCA reduces the risk of investing a large sum just before a market drop; it helps smooth out the entry price over time.

- Lump Sum can be more efficient if you have a large amount to invest immediately, especially in a rising market,but it’s riskier emotionally.

Why DCA Suits Beginners

- Encourages discipline.

- Mitigates the fear of “buying at the top.”

- Makes investing predictable and automatic.

Rebalancing

Once a year:

Return to your target allocation.

WHY:

Over time, some assets will outperform and grow faster (say, stocks), while others lag (like bonds). This changes your original allocation and risk profile.

For example, if your target is 60% stocks / 40% bonds, you might rebalance if stocks grow to 65% or drop to 55%.

Rebalancing forces discipline: you’re effectively “locking in gains” and “buying low.”

Biggest Enemy: Your Emotions

Markets will crash again.

Always.

Winners:

- stay invested

- buy more

- ignore noise

Losers:

- panic sell

- chase hype

- jump in & out

The challenge is to stay the course rather than reacting emotionally.

Staying the Course

- Historical data supports that time in the market beats timing the market.

- Use strategies like DCA and automatic investing to remove emotion.

- Keep a long-term perspective: market downturns can be opportunities, not reasons to exit.

Taxes in Kenya (Simple)

- Capital gains tax: 15%

- Dividends taxed

- Bonds taxed

Use pension & long-term accounts to reduce taxes.

Your 2026 Beginner Action Plan ✅

- Build emergency fund (MMF- Money Market Fund)

- Pay off expensive debt such as mobile loans and credit cards.

- Define your investment goal

- Choose Investing platform (Hisa, Ndovu, etc)

- Start with low-risk investments (Beginner Zone)

- Buy index fund / robo portfolio/ Target Fund

- Move to growth investments (Once comfortable and you understand basics and consistency.)

- Government Bonds & Treasury Bills directly via CBK DhowCSD Or through a bank/investment firm

- Consider long-term & alternative options such as Retirement Schemes and Real Estate.

- Automate monthly investing

- Be consistent

- Avoid common beginner mistakes

- Review once a year

That’s it.

No complexity needed.

By following this beginner’s guide to investing in 2026, you avoid common mistakes and build a system that grows with you over time.

Common beginner mistakes to avoid🚫

- Chasing “quick returns”

- Investing money you’ll need soon

- Copying friends blindly

- Ignoring fees & risks

- Putting all money in one place

Tools for Gen-Z Investors

Budgeting

- Money Manager

- YNAB

- Notion templates

Tracking

- Google Sheets

- Ndovu dashboard

- Personal Capital

Learning

- The Simple Path to Wealth by JL Collins – Evergreen advice on investing for freedom.

- A Random Walk Down Wall Street by Burton Malkiel – A classic for understanding markets and efficient investing.

- YouTube: Plain Bagel, Patrick Boyle, Two Cents